The EU Loses Ground to the US and China

When we talk about power in the 21st century, we first think of armies, GDP, or diplomatic influence. But beneath these perceptions rooted in long tradition lies a less visible yet far more relevant conflict today: the one taking place in laboratories and research centers, where the real decisions are made about who will dominate the economy and geopolitics of the coming decades. Research and development are no longer mere instruments of state power—they have become the very substance of that power.

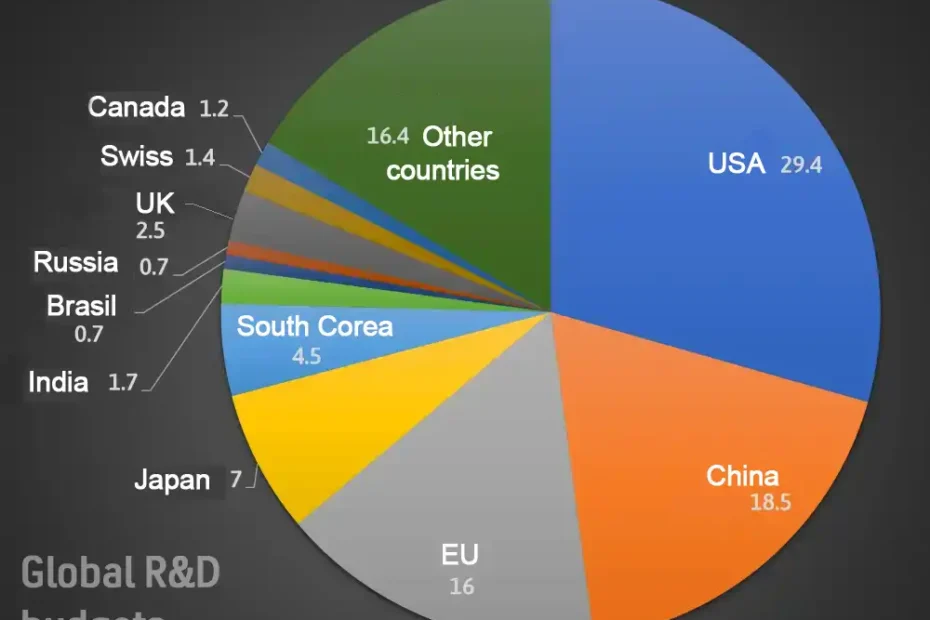

Global Hierarchy

The numbers paint a troubling picture. In 2025 (estimated), global spending on research and development approaches $2.8 trillion, a sum exceeding the GDP of most countries worldwide. Of this ocean of resources, the United States controls approximately 29%—nearly $823 billion—maintaining its position as the undisputed leader. China, with spectacular growth over the past decade, now holds between 18 and 20% of global spending, representing $500-560 billion. Between these two giants, the European Union sits on a lower rung, with a share of 15-17%, equivalent to $420-480 billion.

| Country/Region | Estimated Share (%) | Estimated Value (billion USD) |

| 🇺🇸 United States | ~29.4% | ~823 |

| 🇨🇳 China | ~18-20% | ~500-560 |

| 🇪🇺 European Union | ~15-17% | ~420-480 |

| 🇮🇱 Israel | ~5.5% | ~155 |

| 🇯🇵 Japan | ~7% | ~200 |

| 🇰🇷 South Korea | ~4.5% | ~125 |

| 🇬🇧 United Kingdom | ~2.5% | ~70 |

| 🇮🇳 India | ~1.5-2% | ~40-50 |

| 🇨🇭 Switzerland | ~1.2-1.5% | ~35-42 |

| 🇨🇦 Canada | ~1.2% | ~33 |

| 🇧🇷 Brazil | ~0.8-1% | ~22-28 |

| 🇷🇺 Russia | ~0.6-0.8% | ~17-22 |

| 🌍Rest of the world | ~13-15% | ~370-420 |

Total: ~100% of 2.8 trillion USD

Europe’s Relative Decline

This hierarchy isn’t just about economic statistics. It reflects a profound geopolitical reality: Europe, once the center of global innovation, is now witnessing its own relative decline. In 2023, the European Union spent €381.4 billion on research and development, with the private sector representing 66% (€253.1 billion). It’s an impressive sum in absolute terms, but increasingly small compared to the growth rate of its competitors.

The pandemic has accentuated this tectonic shift. Brexit shattered the European research bloc, and the United Kingdom, which contributed substantially to the continent’s innovation capacity, now reports data separately. China, meanwhile, has dramatically accelerated its investments, exceeding not only expectations but also the forecasts of the most optimistic (or pessimistic?) Western analysts. The result? The European Union has dropped to third place globally—a position that would have seemed unimaginable just two decades ago.

But more concerning than the ranking itself is the internal structure of European research. Unlike the United States and China, where innovation concentrates in rapidly growing sectors like biotechnology and the digital economy, Europe remains anchored in medium-technology industries, especially the automotive sector. Even when research leads to practical applications (patents and startups), their potential to generate productivity is limited compared to the domains targeted by Americans and Chinese.

High-Tech Geopolitics

This concentration on the automotive industry is no accident. Germany, France, and Italy—the three economic pillars of the Union, representing over 60% of European wealth—have deep histories tied to automobile production. But what was once a major competitive advantage is now becoming a strategic vulnerability in a world where artificial intelligence, biotechnology, and green technologies define the economic future.

Germany remains the colossus of European research, holding nearly half of all Union biotechnology patents alongside France. Berlin invests massively in energy transition and advanced manufacturing technologies, attempting to reinvent its industrial model built on combustion engines. France, in turn, bets on an ambitious mix combining nuclear energy with the aerospace and pharmaceutical biotechnology sectors. Italy, though less visible in global rankings, concentrates its efforts on industrial design, automation, and biopharmaceuticals.

But such national efforts, however impressive individually, fail to compensate for the lack of a coherent European strategy. As French Finance Minister Bruno Le Maire acknowledged, everyone has an economic strategy except Europe. It’s a troubling diagnosis for a continent that built its identity on the idea of unity and cooperation.

The Horizon Europe program, with a budget of €95.5 billion for 2021-2027, represents Brussels’ attempt to coordinate research efforts at the continental level. It’s the world’s largest research program, a true bureaucratic behemoth funding projects in every imaginable domain. But this budget size doesn’t guarantee efficiency. Mario Draghi’s September 2024 report on European competitiveness warns that the Union must increase R&D spending to €750-800 billion annually if it wants to remain relevant. In other words, Europe must double its investments (as union and as nations) just to avoid losing even more ground.

European research priorities reflect both the continent’s aspirations and constraints. Medicine and public health occupy a central place—a natural legacy of developed social systems and an aging population requiring constant medical innovations. Green technologies and sustainability aren’t just passing trends—they represent an existential necessity for a continent that has assumed the role of global leader in fighting climate change. The automotive industry and smart mobility complete the trio of priorities, though here Europe finds itself in a race against time to avoid losing supremacy to Asian electric vehicle manufacturers.

Aggressive Development

Unlike these relatively conservative strategic choices, Europe’s competitors have adopted far more aggressive approaches. The United States dominates artificial intelligence, biotechnology, and the defense sector—domains that not only generate enormous profits but also shape the rules of the global economic game. China has made an even clearer choice: artificial intelligence, robotics, telecommunications, and semiconductors—all the sectors that define the economy of the future. Beijing isn’t satisfied with being competitive; it wants to establish the technological standards of the 21st century.

This contrast becomes even more evident when we look at the global distribution of research priorities. Artificial intelligence is the domain with the broadest global coverage, being a priority for the United States, China, South Korea, the United Kingdom, Canada, and Japan. Europe, though present in this race, doesn’t rank among the leaders. In semiconductors—the fundamental component of any modern technology—leadership belongs to South Korea, Japan, China, and the United States. Europe remains a net importer, a strategic dependency that becomes increasingly problematic as geopolitical tensions rise.

Main Research and Innovation Domains:

USA: Information technology and artificial intelligence • Health and biotechnology • Defense and aerospace

CHINA: Artificial intelligence and robotics • Energy technologies (including green and nuclear energy) • Telecommunications and semiconductors

EUROPEAN UNION: Medicine and public health • Green technologies and sustainability • Automotive and smart mobility

SOUTH KOREA: Semiconductors and displays • Artificial intelligence and 5G • Electric automotive and batteries

UNITED KINGDOM: Biotechnology and health • Artificial intelligence and fintech • Renewable energy and environment

JAPAN: Electronics and semiconductors • Automotive and robotics • Medicine and elderly care

CANADA: Medicine and health • Green technologies and natural resources • Artificial intelligence and robotics

INDIA: Information technology and software • Space and defense • Biotechnology and agriculture

SWITZERLAND: Pharmaceuticals and biotechnology • Medical technologies • Finance and cybersecurity

RUSSIA: Defense and aerospace • Energy (oil, gas, nuclear) • Dual-use technologies (civilian-military)

ISRAEL: Digital technologies and artificial intelligence • Biotechnology and medicine • Dual-use technologies (civilian-military)

BRAZIL: Agriculture and bioeconomy • Public health and tropical diseases • Energy (including biofuels)

There are domains where Europe maintains its leadership position. Health and biotechnology represent the continent’s strong points, with centers of excellence in Switzerland, Germany, France, and the United Kingdom. European pharmaceutical firms, from Roche to Novartis, from Sanofi to AstraZeneca, continue producing innovations that save lives and generate considerable profits. Green technologies and renewable energy are other areas where European expertise remains indisputable, fueled both by the real need for energy transition and strict carbon emission regulations.

The Venture Capital Gap

But these partial successes cannot hide a broader and more troubling reality. The gap in funding for European companies in the expansion phase is enormous compared to the United States—only 5% of global venture capital funds are directed to the European Union, versus 52% in the United States and 40% in China. This discrepancy doesn’t reflect a lack of ideas or talent in Europe, but rather a fragmentation of capital markets and a cultural aversion to risk that prevents transforming basic research into global companies.

The problem isn’t technical, but profoundly political and cultural. Europe has prestigious universities, world-class researchers, and powerful multinational companies. But the ecosystem that should connect these elements doesn’t function optimally. Reducing intra-European sectoral barriers to the level observed between American states could increase productivity by 6.7%, according to International Monetary Fund estimates. In other words, Europe sabotages itself through the fragmentation of its markets and administrative borders.

The China Dilemma

The complex relationship with China adds another dimension to this equation. In the Horizon Europe 2021-2022 programs, Brussels introduced protective measures for sensitive technologies, and in the 2023-2024 programs, specific limitations regarding China were added for market-close actions. It’s a delicate balance between beneficial scientific cooperation and protecting competitive advantages, between openness to global talents and strategic security.

This ambivalence reflects a broader dilemma facing Europe: how to remain open and liberal in an increasingly protectionist and strategic world? The United States has adopted a clear approach through the CHIPS and Science Act and restrictions on exports of advanced technology to China. Beijing, in turn, doesn’t hesitate to use massive industrial policies to support its companies. Europe, caught between its liberal principles and economic security imperatives, hesitates, negotiates, postpones, compromises.

The consequences of these hesitations are already visible. In artificial intelligence, European companies are massively outpaced by American and Chinese giants. In semiconductor production, the continent has become dangerously dependent on Asian supply chains. In digital platforms, from social networks to cloud services, American firms dominate. Europe has transformed, almost without noticing, from a technology creator into a consumer and regulator of technology created elsewhere.

The European Paradox

The European paradox thus becomes increasingly evident: the continent that gave the world the Industrial Revolution, that invented the combustion engine and antibiotics, that miraculously rebuilt its economy after World War II, now seems incapable of generating major waves of innovation. Not from lack of financial resources—budgets remain impressive. Not from lack of talent—European universities continue to train exceptional researchers, many of whom then leave for Silicon Valley or Chinese tech centers. But from lack of strategic coherence, risk-taking, and political will to transform research into real economic power.

The cumbersome decision-making mechanism (through a multitude of national and community filters) and political-electoral vulnerabilities at each member state level create real difficulties in defining and pursuing strategic priorities. As the EU currently functions, it faces real challenges in defending its geopolitical position, its economic standing, and ultimately, its prosperity. And it took Trump’s decisions for the EU to realize that, although the partnership with the US will continue in the medium term, Europe is ultimately on its own in the contemporary world. And that it can no longer consider American scientific and technological progress as belonging to the entire North Atlantic alliance.

The future of the entire geopolitical picture depends on Europe’s capacity to reinvent its innovation model and become relevant again in R&D. The question isn’t whether the Union has resources or talent—the answer is obviously affirmative. The real question is whether the Union’s fragmented political system can generate the coherence and speed necessary to respond to 21st-century challenges. Because in the global race for innovation (and economic competitiveness), third place isn’t a bronze medal. It’s just a step separating you from the category „Rest of the world.”